COMMERCIAL SOLUTIONS AND CARD PAYMENTS - SYDNEY, AUSTRALIA

Where commercial payments expertise becomes your competitive edge.

Experienced independent consultant specialising in commercial payments and card programme strategy.

300+

VCN IMPLEMENTATIONS GLOBALLY

$500M

MONTHLY SPEND UNDER MANAGEMENT

50+

BANKS ENGAGED WORLDWIDE

25+

YEARS IN PAYMENTS

Senior counsel.

Specialist practice.

Accountable delivery.

Independent. Objective. Precise.

01 Bank Economics.

The commercial charge card is one of the most capital-efficient working capital product on a bank's balance sheet. Under Basel III, correctly structured charge card programmes qualify for a 45% transactor risk weight — compared to 100% for unsecured lending. The programme economics work for the bank, the buyer, and the balance sheet simultaneously.

02 Working Capital Transformed.

A correctly structured commercial charge card programme converts accounts payable from a cost centre into a working capital instrument. The 45 to 55 day payment float delivers effective financing at a rate below every conventional working capital product available to businesses — with zero collateral and zero personal guarantee.

03 Expertise — Designed. Deployed. Delivered.

Advisory without implementation is incomplete counsel. At CSCP every engagement ends with a working programme. Not a recommendation. Not a framework. A live performing result that banks and corporates can measure, operate and grow.

04 AP Reimagined — Uncaptured. Untapped. Unrealised.

Most organisations have a card programme. Few have maximised it. The majority of AP spend — supplier invoices, contractor payments, recurring obligations — remains outside the card environment. Uncaptured. Untapped. Unrealised. The commercial opportunity sitting inside your existing AP function is material. CSCP identifies it, structures it and converts it.

05 Travel — Unchecked. Unified. Reconciled.

Travel spend happens before anyone can control it — distributed across every employee and booking, policed only after the fact. The same working capital inversion that applies to AP applies here: the same float, the same sub-market financing. But travel carries a second cost most programmes never solve — reconciliation, traditionally the most manual category in AP. CSCP closes both gaps at once: the card's working capital advantage, and automatic reconciliation straight to the journal.

PRACTICE AREAS

Four disciplines. One practice.

01

Commercial Card Strategy

Define and execute a card programme strategy that converts your AP spend into a working capital advantage. Built on commercial mechanics, not generic consulting frameworks.

For CFOs and finance directors, this means a structured reduction in working capital costs, improved cash flow visibility, and a card programme that captures significantly more AP spend than conventional corporate card deployments.

03

Financial Reconciliation

Accurate financial reconciliation requires a data architecture that connects daily transaction records to end-of-cycle statements — automatically and without manual intervention.

CSCP designs and delivers customisable reconciliation output architecture across a wide range of ERP and financial management systems — including journal files and formats compatible with the corporate's existing financial infrastructure.

02

Payments & ERP Integration

A card programme that does not integrate with the corporate's infrastructure is a programme that will not scale. CSCP designs and deploys card programmes with live connectivity across enterprise systems — delivering full Level 2/3 data capture, automated reconciliation and real-time spend reporting from day one of deployment. Every integration is architected to operate within the corporate's existing payment infrastructure and procurement workflows — not around them. The result is a programme that is embedded, operational and generating returns from the point of go-live.

04

Issuer Advisory to Launch

Launching a commercial card programme requires deep understanding of scheme architecture, regulatory capital, programme economics and the operational infrastructure needed to support it from day one.

CSCP advises issuing banks from initial programme design through to live launch — covering scheme integration, pricing design and the operational framework required to run a sustainable, capital-efficient programme at scale.

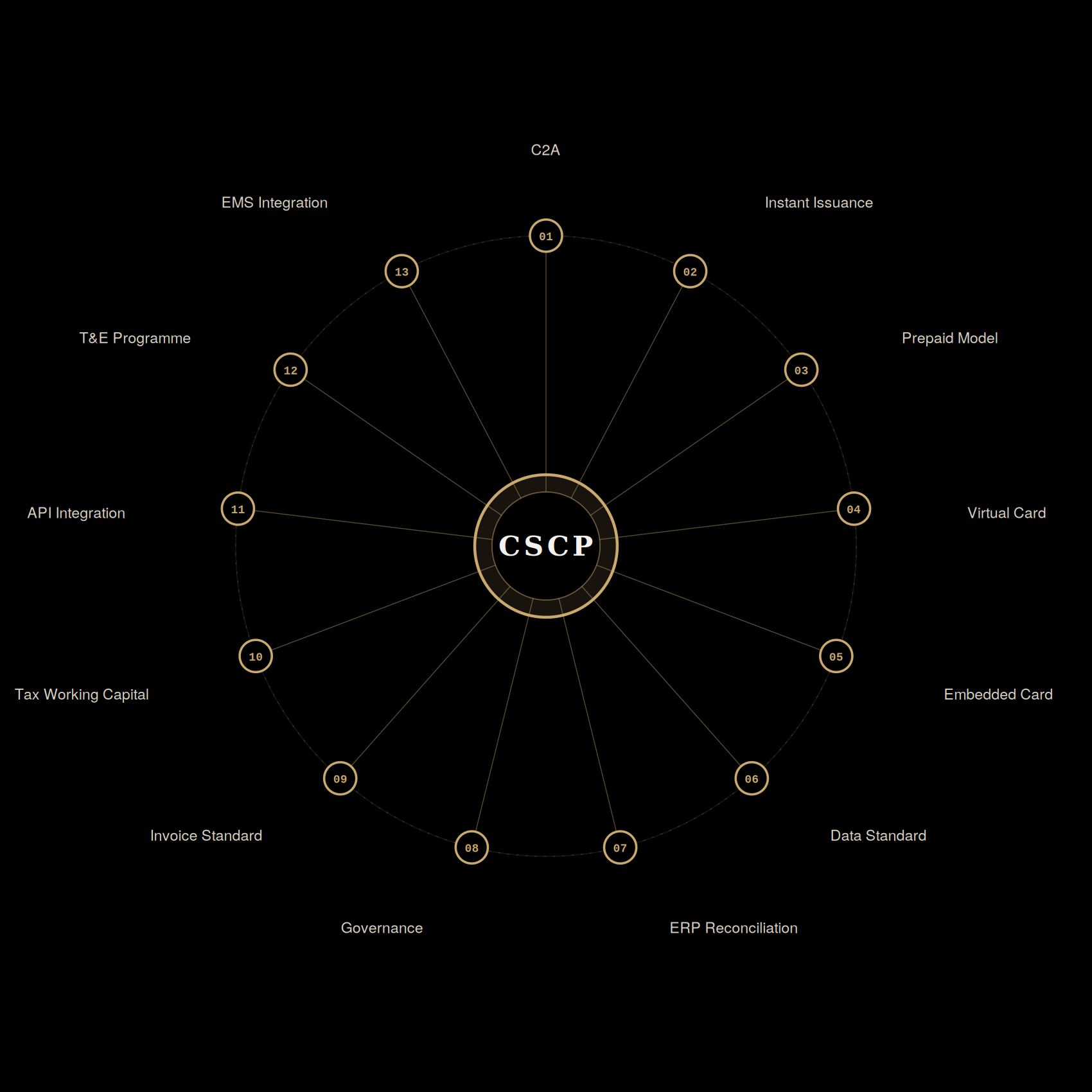

13 frameworks.

Built from implementation, not theory.

Every CSCP framework has been stress-tested across live bank deployments, enterprise implementations, and regulatory environments spanning global markets. These are not consulting models — they are operational tools refined over 300+ implementations and 25 years of practitioner experience.

"Systematic, repeatable methodology is what separates a practice from a practitioner. CSCP's 13 frameworks represent the codified knowledge of a career spent inside the system."

FRAMEWORK 01

Card to Account Payment Architecture

A payment architecture that enables card-funded payments to be settled directly to a supplier's bank account via domestic payment rails eliminating the requirement for supplier card acceptance while preserving the buyer's card float and programme economics.

FRAMEWORK 03

Credit Powered Prepaid Model

A virtual card presented to the end user as a standard prepaid instrument, while the underlying facility draws against a credit card rather than pre-funded cash — delivering the working capital advantage of credit-based spending without the cash-lockup cost structure inherent to genuine prepaid programmes.

FRAMEWORK 05

Embedded Virtual Card Program

Virtual card issuance and payment triggered natively within an enterprise procurement or invoice-approval platform — the card exists only as an embedded payment mechanism inside an existing workflow, not as a separate programme the client has to adopt or manage.

FRAMEWORK 07

ERP Reconciliation Blueprint

Maps card transaction data directly to general ledger posting logic across major enterprise resource planning platforms, using merchant category code mapping to assign client-specific GL codes automatically at the point of transaction — with exception handling for unmapped or ambiguous codes, and enhanced transaction-level data enrichment throughout. Built for procurement and accounts payable card spend with no manual claim or approval step required.

FRAMEWORK 09

Universal Invoice Card Payment Blueprint

Detects supplier-authorised card payment terms across any invoice source — Peppol, EDI, or government-mandated e-invoicing platforms — and routes consenting invoices to CSCP's virtual card programme, with invoice data mapped directly into the card at the point of generation for direct journal posting with no manual reconciliation. Validated across fifteen-plus global markets spanning five continents.

FRAMEWORK 11

Commercial Card API Integration Framework

Technical integration expertise for connecting clients directly to commercial card scheme APIs — programme management, transaction data, and virtual card generation — enabling SaaS platforms, large corporates, fintechs, and banks to build directly on card network infrastructure rather than through legacy host-to-host connections.

FRAMEWORK 13

EMS Integration Blueprint

Routes T&E and employee card spend through an expense management system — expense claim creation, receipt capture, policy check and approval workflow — before posting to the general ledger, with the human-submitted claim and approval step built into the flow as a core requirement rather than an exception.

FRAMEWORK 02

Mobile Instant Issuance Framework

Instant card issuance directly into a mobile wallet for non-standard, often one-time recipients — contractor payments, transport vouchers, airline disruption compensation — where no prior cardholder relationship exists and a physical card is neither possible nor practical.

FRAMEWORK 04

Virtual Card Implementation Architecture

End-to-end blueprint for virtual card programme deployment — from ERP integration through supplier settlement to automated reconciliation, with full transaction-level data capture across major enterprise resource planning platforms.

FRAMEWORK 06

Card Program Data Standard

Specification framework for the complete financial data layer of a card programme — covering card transactions, issuer fees and automatic payments, account-to-account transfers, and programme economics data, parsed and field-mapped from the underlying settlement file format into structured, usable intelligence.

FRAMEWORK 08

Program Governance Framework

Policy, control and reporting structure for enterprise commercial card programmes, covering spend limits, approval hierarchies and compliance monitoring — aligned to corporate treasury governance requirements and regulatory obligations specific to each operating jurisdiction.

FRAMEWORK 10

Card-Funded Working Capital Model for Tax Payments

Applies the working capital inversion principle to statutory tax obligations — funding tax payments via commercial card to capture the payment float. Where a card surcharge applies, the framework benchmarks the all-in cost against the float benefit on an annualised basis; where surcharging is removed or restricted, as regulatory reform increasingly provides for, the float benefit applies with no offsetting cost. Modelling is calculated per engagement, against the rates and regulatory settings of the relevant jurisdiction. This framework involves indicative cost modelling only and does not constitute financial, tax or legal advice.

FRAMEWORK 12

T&E Card Programme Framework

Design and implementation of travel and expense card programmes. Of every commercial card product in market, the physical corporate card remains the most widely deployed instrument for T&E spend — policy design, control limits, and merchant category restrictions built around this core instrument.